This content was contributed by Manulife Investment Management (Singapore) Pte. Ltd

How retirement investments align with long-term sustainability goals

03 June 2024 | 8 mins-read

A commonality between a typical portfolio for retirement and a sustainable investor is that both share a long-term horizon, seeking to achieve defined objectives over the course of many years—even multiple decades. In this piece, we focus on how investment portfolios can be built to align with the important and financially material sustainability themes.

Taking the long-term view

A commonality between a typical portfolio for retirement and a sustainable investor is that both share a long-term horizon, seeking to achieve defined objectives over the course of many years—even multiple decades.

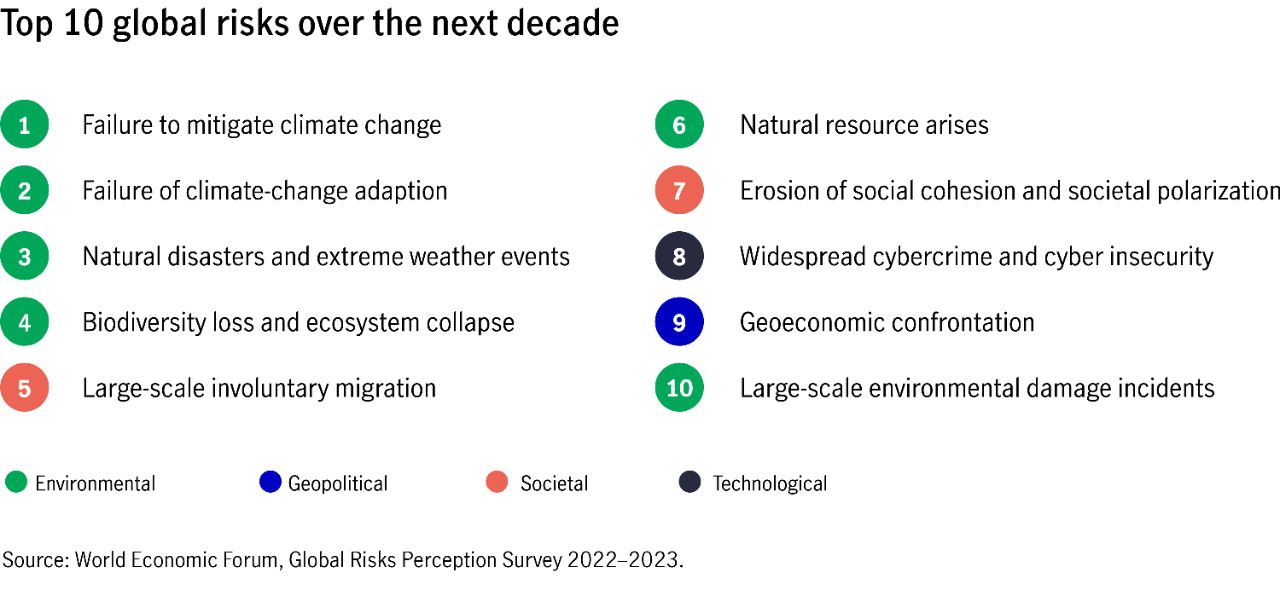

The World Economic Forum Global Risk Report 2023 states that 8 of the top 10 risks over the coming 10-year period are environmental and societal related, and the timeframes for making fundamental changes to avoid significant economic and social damage from climate change and nature collapse are closing.

Indeed, investment portfolios focused on long-term return objectives will be less likely to achieve them if climate-change mitigation and nature and biodiversity regeneration are not also achieved on a global scale. In this piece, we focus on how investment portfolios can be built to align with these important and financially material sustainability themes.

Climate change as an example for risk and opportunity in retirement asset allocation

Unanimous scientific agreement tells us that humans have emitted enough greenhouse gasses (GHGs) over the last century, and mostly in the last 30 years, to warm the planet just over 1°C above preindustrial levels. If we carry on business as usual with this level of emissions, we'll cause the planet to warm about 4.5°C on average by 2100.

Sophisticated modeling of climate change reveals that it's virtually certain to lead to dramatic results. Heavily populated coastal regions on multiple continents could be submerged by rising seas, or at least subjected to far more severe storm surges during major weather events. Other areas of the planet could be rendered uninhabitable due to extreme heat, severe freshwater stresses, or increased storm intensity.

To avoid the worst of these physical risks, nearly every government on Earth signed the Paris Agreement in 2015, where signatories agreed to reduce their GHG emissions to a level that would hold global warming to 1.5°C and well below 2°C above preindustrial levels. But to make this happen will require transformational changes to the way societies and economies work. Virtually every sector is currently dependent on fossil fuels in one way or another. Moreover, developed-market economies are commonly habituated to outsized levels of consumption relative to emerging markets, and so replacing fossil fuels with renewables to support today's baseload energy requirements will be no small task.

To achieve their GHG reduction targets, countries are setting "net zero by 2050" goals and developing low-carbon policies and incentives to accelerate their progress. Companies' products, services, and operations can be affected by these policies, and so companies, in turn, are setting their own net zero targets. By focusing on these company-level objectives, investors—and their plan sponsor partners—have the opportunity to assess how their portfolios can align capital with net zero targets.

Measuring the relative preparedness and resilience of different asset classes

Next, we take a look at how different asset classes are generally positioned relative to net zero by 2050 targets, as well as options for decarbonising broader portfolios.

When investing through the lens of climate risk, the first step is to understand the impact that climate change has had or is likely to have on an asset or an issuer's business, as well as the impact that the asset or issuer may have on the climate. Although this can be a complex assessment, two high-level metrics that are useful for measuring these dual impacts—and by extension the relative preparedness and resilience of different companies—are the presence of disclosures and targets: specifically, whether a company has:

- Measured and reported on its scope 1, scope 2, and scope 3 emissions1

- Set a net zero by 2050 target

Using these data points as proxies for preparedness and resilience in the face of both climate change and the transition to a lower-carbon economy, we can assemble asset-class-based measures of the same using broader market indexes.

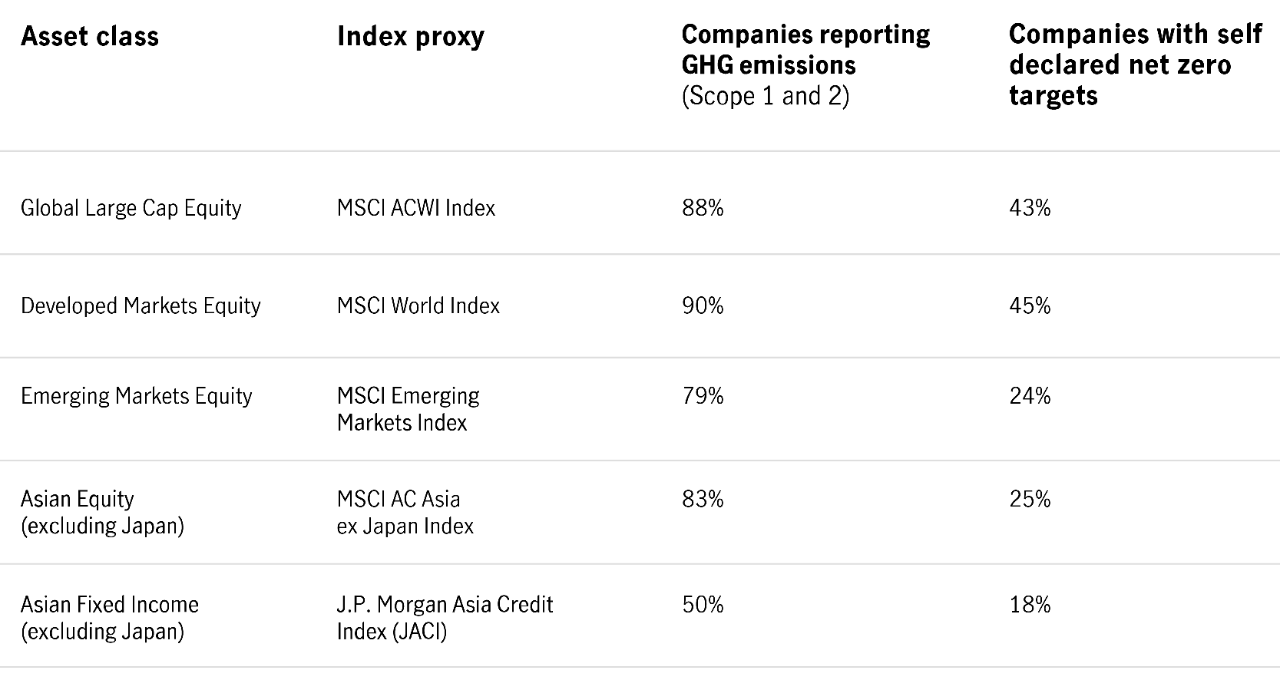

Prevalence of net zero targets among major asset classes

Source: Manulife Investment Management, Bloomberg. Data as of December 31, 2023. The MSCI All Country World Index (ACWI) tracks the performance of large-and mid-cap stocks of companies in developed and emerging markets. The MSCI World Index captures large and mid-cap representation across 23 Developed Markets (DM) countries. The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. The MSCI AC Asia ex Japan Index captures large and mid-cap representation in Asia excluding Japan. The J.P. Morgan Asia Credit Index (JACI) is an all inclusive benchmark that tracks liquid, US-dollar denominated debt instruments issued out of the Asia ex-Japan region. The index includes debt issued by Corporate, Sovereign, and QuasiSovereign entities from the region spanning both Investment Grade and High Yield debt segments.

On this view, developed markets equity and global large-cap equity are ahead of other asset classes when it comes to measuring their scope 1 and scope 2 emissions as well as net zero target setting. This is supported by the prevalence of mandatory environmental information disclosure for listed companies and governmental climate commitments in those countries. Although the GHG emission reporting by the listed companies in the emerging markets and Asian region is closely following to their peers in the developed markets, we observe a lower rate of net zero target setting for both EM & Asian equity and fixed income asset classes, partly due to varied net zero target timelines and related policy frameworks among the Asian governements. Notably, China and India, the two emerging economies in this region, deviate in their net zero target from 2050 to 2060 and 2070 respectively. Sovereign issuers, subsovereign issuers, and other government-owned corporate issuers from the two economies, comprising a major part of the Asian fixed income asset class, tend to align their climate strategy with their respective goverments’ commitment. That said, these two economies also lead the investment into clean technologies in the region.

Aligning equities and fixed-income investments with climate and sustainability goals

There are a number of ways equity and fixed-income investment managers can align with a net zero by 2050 target, or take advantage of risks and opportunities arising from the transition to a low-carbon and sustainable economy. By extension, pension schemes and administrators can assess different strategies' alignment by considering whether they:

- Invest in climate and sustainable leaders — Investors can focus on companies deemed to be leading the low-carbon transition and/or the management of sustainability issues whether in their products and services or in the way they operate. Opportunities are opening up as the cost of renewable energy declines, as advances in technology (including battery storage, electric vehicles) emerge, as regulations change, and as a result of shifting consumer and employees expectations. Some companies are ramping up their cleantech revenue, while others are finding ways to shift off fossil fuels at scale and/or decarbonise through their value chains whilst others are leading in their human capital management and diversity, equity, and inclusion (DEI) practices.

- Invest in the enablers for a low-carbon economy and sustainable development — Investors can seek out opportunities that are contributing to the low-carbon economy including renewable power generation, low-carbon transportation, green buildings, renewable power generation and technology. In addition, investment into products and services that address economic empowerment and demographic transition including healthcare and pharmaceutical, education, fintech and insurance services.

- Invest in the ESG-labeled bond market — Green, social, sustainable, and transition bonds make up a new and fast-growing market segment. The labeling of these bonds should correspond to international standards and/or be reviewed by a third party. Often, they're linked to the issuer meeting environmental and/or social objectives through the use of proceeds (i.e., the issuer specifies that the funds will be used for decarbonization projects) or through terms and conditions (i.e., if prespecified sustainability targets such as emissions reductions aren't met, the investor is compensated additional basis points).

- Engage with or avoid laggards — Other options include engagement: working with companies lagging on their climate actions or sustainable business practices to help them set and begin acting on credible transition plans. When such plans are slow in coming, are insufficiently robust, or fail to materialise, a strategy of escalation may be appropriate. This can involve speaking directly to boards of directors, voting on or filing shareholder proposals related to climate risk, and, ultimately, reducing exposure to or avoiding laggards when management fails to reform its business practices.

There are several different reasons to align with a net zero by 2050 investment strategy, ranging from avoiding the weaker performances on ESG issues; aligning with, and accelerating, the low-carbon transition and sustainable development; and capitalising on opportunities in companies that are positioning themselves to be more competitive in a low-carbon and sustainable future.

Sources

1 Scope 1, 2, and 3 are categories for an organisation's greenhouse gas emissions. Scope 1 refers to direct GHG emissions from company-owned sources (e.g., fuel combustions in vehicles and factories, and fugitive emissions). Scope 2 encompasses indirect emissions associated with the purchase of electricity, steam, heat, and cooling needed by the company to operate. The two reporting methods of Scope 2 emissions are the market-based method, which is based on the electricity that a company purchases and its use of green energy tariffs such as Renewable Energy Certificates, and the location-based method, which measures how much emissions are physically put into the air based on the company's average emission intensity from its power grid. Scope 3 covers all indirect emissions linked to the company's operations that aren't included in Scope 2. There are upstream Scope 3 emissions which come from the production of a company's products or services, while downstream emissions come from their distribution, use, maintenance, and disposal. From employees' business travel and commute transportation to waste management, Scope 3 is the hardest to assess, yet in most cases, it represents the biggest GHG impact.

Important note:

The information provided on this website is for informational purposes only and is intended solely for use by Singapore residents and is not intended for distribution to, or use by, any person or entity in the United States, or any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G), Manulife (Singapore) Pte. Ltd. (Company Registration No. 198002116D) and/or its affiliates (collectively hereafter "Manulife") or any of Manulife's products or services to any registration requirement within such jurisdiction or country. Nothing on this website shall be construed as financial advice or an offer, invitation, solicitation or recommendation by or on behalf of Manulife to any person to buy or sell any Fund and is no indication of trading intent in any Fund managed by Manulife. None of the information or analyses presented are intended to form the basis for any investment decision, and no specific recommendations are intended. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Thank you for contacting Manulife Singapore!

Our Financial Consultant will be in touch with you soon.

Here are some links you might find useful.

Consent

By submitting your personal details,

- You acknowledge that you authorise and consent to Manulife (Singapore) Pte Ltd ("Manulife) (including employees and Representatives of Manulife) to collect, use, disclose and retain your personal data for the purpose of receiving notifications via SMS(es) and email(s) to service your request; and

- You consent to Manulife to contact you (even though your telephone number may be already registered on the National Do Not Call Registry) for marketing purposes, and to provide you with marketing, advertising and promotional information, materials and/or documents relating to financial advisory services and products distributed by Manulife, if applicable.

The consent you provide is in addition to and does not supersede, vary or nullify any consent which you may have provided previously in respect of the above purposes, unless your previous consent has been withdrawn.

You also confirm that you are the user and/or subscriber of the telephone number and email address provided by you.

More Insights you might find interesting

Actively plan and smooth your way to retirement

Your retirement withdrawal strategy - four tips for managing inflation